Zhengzhou Cotton Prices Retreat from High Levels, While U.S. Cotton Soars! A Xinjiang Textile Industrial Park with a $2-Billion Investment Breaks Ground; Tianhong International’s Net Profit Grew by 63% Last Year!

1. Domestic cotton prices fluctuate at a high level and slightly fall back

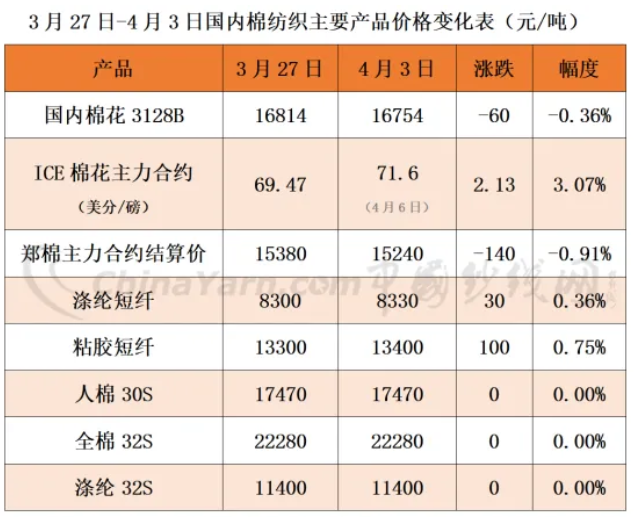

Last week, due to the resilience of downstream consumption and expectations of a contraction in supply for the new year, as well as the support of traditional peak seasons such as gold, silver, and textile raw material replenishment, "gold, silver," and "silver" have landed, and downstream demand has slowed down. However, the market's expectation of tight supply for the next year is still strong, and the overall narrow fluctuation of domestic cotton prices has fallen. The local price of Xinjiang cotton to the factory in Hebei region is about 16900-17100 yuan/ton, slightly lower than the previous two days. On April 3rd, the domestic cotton 3128B price index was 16754 yuan/ton, a decrease of 0.36% from last week; The settlement price of Zheng cotton's main contract is 15240 yuan/ton, a decrease of 0.91% compared to last week.

2. New York cotton futures prices rise sharply

Last week, the preliminary planting area report of the US Department of Agriculture (USDA) was released, and the shipment data of US cotton export contracts rebounded. From the report, it can be seen that China's increase in quotas has significantly increased the number of US cotton contracts, and the market continues to be optimistic about the demand for US cotton exports in the later stage. In addition, the market is concerned about the dry weather in US production areas and the next round of economic and trade negotiations between China and the United States. The expected reduction in the intended planting area of US cotton, as well as the expectation of global supply tightening this year, have provided some support for cotton prices. On April 6th, cotton futures prices in New York rose sharply, with the main contract reaching a high of 71.93 cents/pound during trading, hitting the highest level since December 2024. On April 6th, the main ICE cotton contract closed at 71.6 cents/pound, up 3.07% from last week.

3. Polyester staple fiber market fluctuates and rises

Last week, the ceasefire agreement reached between the United States and Iran "gradually extinguished hope". There are reports in the market that the final order to strike Iran is expected to be issued on the evening of the 7th Eastern Time. International oil prices have skyrocketed in response, and the Middle East war has been fluctuating. Currently, the polyester staple fiber market is showing a volatile upward trend, and futures performance is relatively strong. On April 3rd, the price of polyester staple fiber was 8330 yuan/ton, up 0.36% from last week.

4. Adhesive short fibers maintain firmness

Last week, there was a strong willingness to raise prices in the adhesive short fiber market. With continuous inventory consumption, the supply side of adhesive short fiber was well supported, and factory quotations were slightly increased. Short term prices continued to remain firm. On April 3rd, the price of adhesive short fiber was 13400 yuan/ton, an increase of 0.75% compared to last week.

5. Textile companies' new orders slightly weaken

Last week, the newly added orders of textile enterprises slightly weakened, and raw material procurement mainly relied on replenishing inventory for urgent needs or buying at low prices. Affected by the slowdown in demand and poor spinning profits, the operating rate of some enterprises in mainland China has declined, and the pace of conventional product sales has slowed down. The market is generally cautious about the purchasing and sales situation in April. On April 3rd, the price of cotton 30S was 17470 yuan/ton, cotton 32S was 22280 yuan/ton, and polyester 32S was 11400 yuan/ton. The prices of the three major yarn varieties remained the same as last week.

6. Market outlook

The repeated escalation of geopolitical conflicts, coupled with persistent concerns about inflation risks in the market, has increased the volatility risk in the commodity market. Although the intended cotton planting area in the United States is higher than expected, international cotton prices have risen strongly due to multiple factors such as the sharp increase in cotton contract volume, worsening drought in major production areas, and soaring international oil prices. The export sales of cotton from the United States have shown strong performance, with the signing volume of upland cotton reaching 84300 tons in the past week (March 20-26), a 94% increase from the average of the previous four weeks, indicating a temporary increase in demand. It is recommended to pay attention to the impact of factors such as spring sowing weather in the northern hemisphere and China US trade negotiations on the market.

Zheng cotton futures prices are under pressure, and external geopolitical conflicts have limited impact on Zheng cotton. The market is focused on domestic new cotton planting, and cotton planting in Xinjiang has started gradually at the end of March. The overall climate conditions have been favorable in recent times. The textile industry is gradually entering the "Silver IV" stage, but the current expectations for it are not high, and there may be a possibility of further weakening. The expectation of tight supply in the new year and the domestic policy of expanding domestic demand provide strong support for the domestic cotton market. The resistance to the upward trend of cotton prices mainly comes from subsequent orders in the textile market and the negative impact of the Middle East geopolitical conflict on the global economy. It is expected to continue to maintain a range oscillation trend in the near future.

2、 Industry operation status

1. ICAC: Global cotton production drops by approximately 4.2% in the new fiscal year

According to the April global cotton production and demand forecast released by the International Cotton Advisory Committee (ICAC), the global cotton production for 2026/27 will be 24.91 million tons, a year-on-year decrease of about 4.2%. China will still be the country with the largest cotton production, expected to reach 6 million tons, followed by India, Brazil, the United States, West Africa, and Australia; The consumption was 25.06 million tons, a year-on-year decrease of about 0.4%; The import volume was 9.65 million tons, a year-on-year decrease of about 2.4%. Among them, China's cotton import volume was 1.1 million tons, a year-on-year decrease of 65%, the lowest level in eight years.

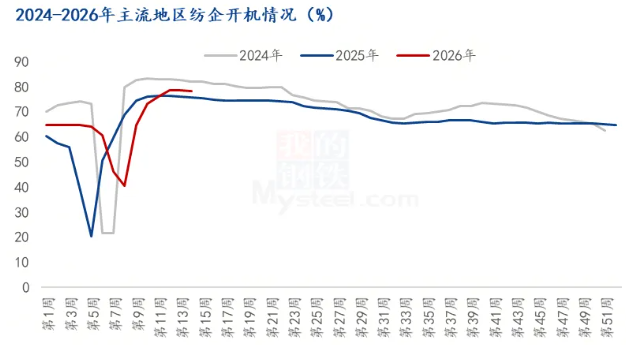

2. The operating rate of textile enterprises in mainstream regions continues to decline slightly

According to Mysteel's agricultural product data monitoring, as of April 2, the operating load of textile enterprises in mainstream regions across the country stood at 78.3%, a decrease of 0.25% from the previous week. Last week, there were limited new orders in the market, and some mainland textile enterprises slightly reduced their operating rates. The operating rate in the Xinjiang region remained above 90%.

3. Enterprise predicts that the cotton yarn market may turn weak in late April

According to the cotton textile market survey released by the China Cotton Industry Association on April 3, the operation of cotton textile markets and related enterprises in various regions is as follows:

Yarn market:

Recently, the trading in the pure cotton yarn market has been weak, with a significant decrease in inquiries and new orders. Textile companies are mainly executing early orders, and some high count yarn varieties are still in short supply. Enterprises generally predict that the market will turn weak in late April; The downstream market has a low acceptance of polyester staple fiber quotations, and the prices of polyester staple fibers have fluctuated and weakened. The prices of polyester containing yarns have also stabilized after falling, and companies are purchasing raw materials at low prices.

Fabric market:

The white fabric market has improved, and the factory opening rate has increased. Fabric factories dare not easily raise prices in order to stabilize orders, and their profits are not ideal due to the increase in raw material prices; The overall market for yarn dyed fabrics is flat, and enterprise orders are mainly small and fast orders, with insufficient follow-up orders.

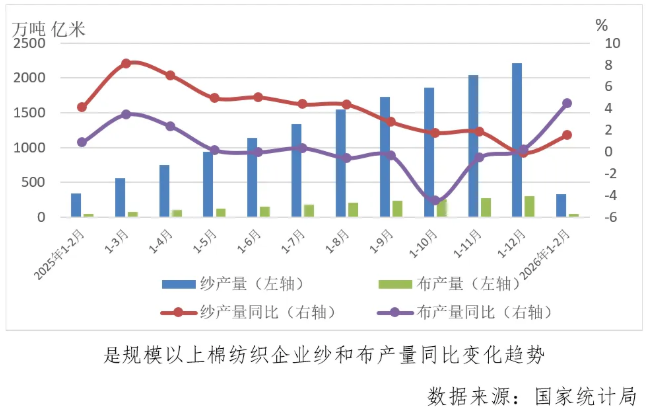

4. From January to February, the yarn production of enterprises above designated size increased by 1.51% year-on-year

According to data from the National Bureau of Statistics, in January and February, the yarn production of enterprises above designated size was 3.308 million tons, a year-on-year increase of 1.51%, shifting from a cumulative decline in the previous year to an increase; The fabric production of enterprises above designated size was 4.36 billion meters, a year-on-year increase of 4.43%, continuing the cumulative growth trend of the previous year, and the growth rate was higher than the yarn production.

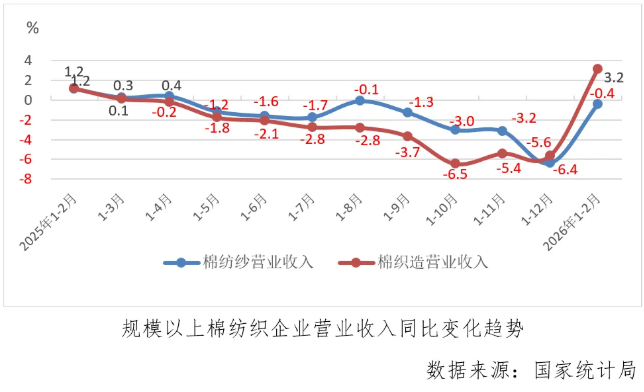

5. The revenue of cotton textile enterprises above designated size increased by 0.8% year-on-year from January to February

According to data from the National Bureau of Statistics, in January and February, the operating revenue of cotton textile enterprises above a certain size increased by 0.8% year-on-year, ending the previous downward trend that had persisted for eight consecutive months. Specifically, cotton spinning revenue decreased by 0.4% year-on-year, marking a significant narrowing of the cumulative decline by 6 percentage points compared to the previous year. Meanwhile, cotton weaving revenue increased by 3.2% year-on-year, turning from a cumulative decline to a growth compared to the previous year.

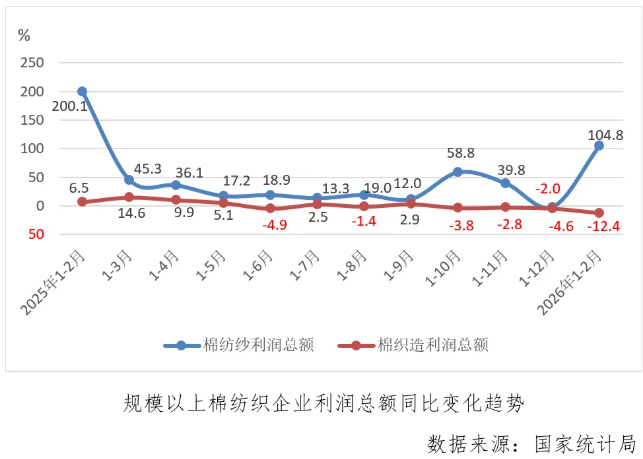

6、1-2月规上棉纺织企业利润总额同比增长18.6%

据国家统计局数据,1-2月份,规模以上棉纺织企业利润总额同比增长18.6%,较上年全年累计下降转为增长。其中,棉纺纱同比大幅增长104.8%;棉织造延续上年全年下降趋势,且降幅扩大了7.8个百分点,达到12.4%。

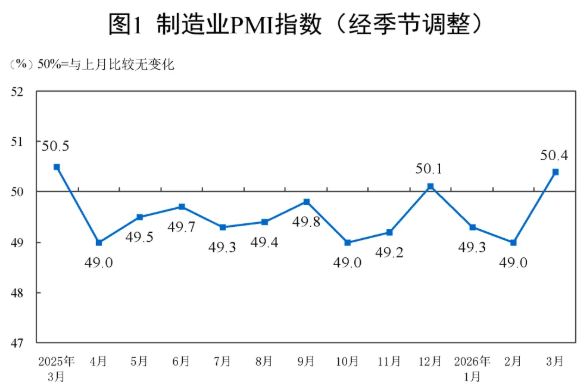

7. The manufacturing industry's prosperity level rebounded in March

According to data from the National Bureau of Statistics, in March, China's Manufacturing Purchasing Managers Index (PMI) stood at 50.4%, marking a 1.4 percentage point increase from the previous month and surpassing the critical threshold, indicating a rebound in the manufacturing sector's economic activity.

3、 Industry Trends and Policies

1. Xinjiang's first "plastic bottle recycling spinning garment" full industry chain connected

On March 27th, with the commissioning of the regenerated polyester staple fiber production line of Xinjiang Chuanmian Textile and Clothing Co., Ltd., the first closed-loop full industry chain in Xinjiang, which includes plastic bottle recycling, regenerated fiber spinning and weaving, printing and dyeing, and garment manufacturing, was fully connected. The total investment of this project is 200 million yuan, with an annual processing capacity of 30000 tons of waste PET plastic bottles. After full production, it is expected to produce 20000 tons of blended yarn, 31.2 million meters of raw fabric, and 110 million meters of printed and dyed fabric annually.

2. The 2 billion yuan all cotton era Xinjiang industrial park project has started construction

On March 28th, the construction of the All Cotton Era Xinjiang Industrial Park project with a total investment of about 2 billion yuan began, of which 400 million yuan is planned to be completed by 2026. This project fills the gap in the high-end cotton non-woven fabric production industry in Xinjiang and injects strong impetus into the high-quality development of the regional economy.

3. Tianhong International and Leica have reached an exclusive cooperation agreement

On March 30th, Leica announced that it had officially signed a strategic cooperation agreement with Tianhong International Group. According to the agreement, Tianhong International Group will reach an exclusive cooperation with Lycra to introduce and promote renewable Lycra containing 30% plant-based ingredients in the Chinese core spun yarn field ® Fiber. This cooperation aims to accelerate the application and development of bio based spandex in the global clothing and textile industries.

4. Xinjiang Yili 450 million yuan flax full industry chain project signed contract

On March 31st, the construction project of the flax full industry chain processing base in Gongliu County, Yili, Xinjiang, with a total investment of 450 million yuan, was officially signed. The project is planned and constructed in two phases. The first phase is an agricultural project with a total investment of 150 million yuan, focusing on the construction of a hemp base with a total area of about 10000 square meters. The total investment for the second phase is 300 million yuan, with a focus on building a pure linen spinning base, covering a total area of about 20000 square meters, including a linen fiber spinning workshop of about 5000 square meters, a textile workshop of 10000 square meters, and a warehousing and logistics warehouse of 5000 square meters.

5. Lanjing expands VEOCEL fiber production capacity in Thailand

VEOCEL, the flagship specialty non-woven fabric brand under Lanjing, has expanded its production capacity at its factory in Prayut, Thailand. This is the first time the brand has achieved localized production of non-woven grade Lyocell fibers in Asia. The project launch ceremony was held locally on March 18th. The factory will be completed in 2022, with an annual capacity of 100000 tons. Previously, it was dominated by textile fiber production. After this expansion, biodegradable wood Lyocell fiber can be stably supplied, covering the core raw material demand of non-woven products such as baby wipes, facial mask and personal hygiene products. This expansion of production can shorten the delivery cycle for Asian customers, ensure supply chain stability, and significantly reduce carbon emissions caused by intercontinental transportation.

6. Weiqiao Textile and Korla Zhongtai Textile have been selected as high-level enterprises with quality management capabilities

Recently, the Ministry of Industry and Information Technology announced the second batch of high-level enterprises with quality management capabilities. A total of 161 enterprises from across the country were listed, including Shandong Weiqiao Textile Technology Co., Ltd. and Korla Zhongtai Textile Technology Co., Ltd., both of which have a certified quality management capability level.

7. Tianhong International's net profit increases by 63% to 913 million yuan in 2025

On March 26th, Tianhong International Group announced its annual performance, with revenue decreasing by approximately 1.4% to approximately RMB 22.7 billion for the year ended December 31, 2025; The profit attributable to the company's owners increased by approximately 63.0% to approximately RMB 913 million. The announcement stated that the performance showed a "deviation between quantity and price": Against the backdrop of market demand recovery, the average selling price of products declined due to pricing competition caused by fluctuations in raw material prices and the trend of "cost-effectiveness" consumption, offsetting the income increase brought by sales growth. During the year, the group is committed to improving existing production capacity, especially the utilization rate of overseas factories, promoting equipment automation transformation, and driving the overall gross profit margin from 12.4% to 13.8%.

8. Meibang Apparel plans to sign a 1 billion yuan procurement contract with related parties

On March 31st, Meibang Apparel announced that the company has entered into a cooperative relationship with its affiliate Guizhou Meibang Xinneng Textile and Clothing Technology Co., Ltd. The company or its subsidiaries will purchase goods from Xinneng Textile, and the expected amount of related party transactions will not exceed 1 billion yuan. If the upper limit amount is reached during the contract period, a new agreement can be signed to increase the upper limit of the cooperation amount.

9. Sun Xiaoting from Huafu Fashion has been elected as the rotating chairman of the Council of China Cotton Association

On March 27th, the China Cotton Association held the third session of the fifth council and the national cotton situation analysis meeting in Shangyu, Shaoxing, Zhejiang. The meeting voted to approve the election of Sun Xiaoting, Vice President of the China Cotton Association and Director and Vice President of Huafu Fashion Co., Ltd., as the rotating chairman of the third session of the fifth council of the association. Wang Jianhong, President of the China Cotton Association, was appointed as the new rotating chairman.

10. The International Textile Capital has been successfully launched

On March 30th, the Zhongke Aerospace Lijian-2 Yao-1 carrier rocket, the International Fangdu, was successfully launched from the Dongfeng Commercial Aerospace Innovation Experimental Zone, delivering the New Journey 01 satellite, New Journey 02 satellite, and Tianshi 01 satellite into their designated orbits with precision. The launch mission was a complete success. The successful launch of the "International Textile Capital" is not only a breakthrough in aerospace technology, but also an important symbol of the industrial level leap in Keqiao District. Keqiao, the "International Textile Capital" with over 8000 textile printing and dyeing enterprises and an annual output value exceeding 150 billion yuan, has sent the business card of a traditional textile city into space, breaking the inherent impression of Keqiao's industry by the outside world.

4、 Domestic and international news

1. Central Bank: We will continue to implement a moderately loose monetary policy and increase efforts in countercyclical and cross cyclical adjustments

The first quarter (112th overall) meeting of the Monetary Policy Committee of the People's Bank of China was held on March 26, 2026. The meeting analyzed the domestic and international economic and financial situation, and believed that the current external environmental changes have deepened their impact, with frequent geopolitical and economic conflicts, differentiated economic performance of major economies, and uncertainty in inflation trends and monetary policy adjustments. We should continue to implement a moderately loose monetary policy, increase efforts in countercyclical and cross cyclical adjustments, better leverage the dual functions of monetary policy tools in terms of quantity and structure, strengthen the coordination of monetary and fiscal policies, and promote stable economic growth and reasonable price recovery.

2. Nine departments jointly issue document to create new consumer scenarios

Recently, the Ministry of Commerce and nine other departments jointly issued the "2026 Work Plan for Improving Service Consumption Quality and Benefiting the People". The plan proposes 64 measures from 6 aspects, covering traditional fields such as catering, elderly care, and cultural tourism, as well as new growth points such as home economics and online audio and video. Both supply and demand sides will work together to create new consumption scenarios and boost the domestic consumer market.

3. The United Nations predicts that the Iran War may cause nearly $200 billion in economic losses to Arab countries

On March 31st, according to an analysis released by the United Nations, the disruption caused by the Iran War could result in a GDP loss of $120 billion to $194 billion for Arab countries. The report states that the overall loss could lead to a maximum increase of 4 percentage points in the unemployment rate in the region, resulting in the loss of approximately 3.6 million jobs and potentially pushing up to 4 million people into poverty.

4. World Data Organization established

On March 30th, the World Data Organization, the world's first professional international organization aimed at promoting data development and governance practices, was officially established in Beijing. At present, the World Data Organization has gathered over 200 members, covering more than 40 countries worldwide. Members include diverse entities such as enterprises, universities and think tanks, international organizations, and financial institutions.

5. The total global public debt has reached $111 trillion

According to data from the International Monetary Fund, the total global public debt will reach $111 trillion by 2025, more than five times the $19.7 trillion in 2000. Among them, the public debt of the United States is as high as $38.3 trillion, while that of China is $18.7 trillion. In addition, Japan's public debt has dropped to $9.8 trillion, partly due to the depreciation of the yen against the US dollar.

6. The Senate's nomination hearing for the Federal Reserve Chairman of Walsh is scheduled for April 16th

On April 4th, according to Politico, Kevin Walsh, Trump's nominee for Federal Reserve Chairman, will attend the Senate Banking Committee's nomination hearing on April 16th. The US Treasury Department has made Walsh's appointment confirmation a top priority. Earlier, it was reported that a federal judge in the United States upheld his previous ruling and refused a request from the Department of Justice to reconsider the ruling against Federal Reserve Chairman Powell.

Please first Loginlater ~